“Insurers need to become catalysts for innovation and government need to spread awareness across each corner of the whole country in order to drive growth in Indian insurance sector”

Even after being the world’s 7th largest country, the second most populous one, the country with the highest number of insurance policies in force and with the total investable funds with LIC which alone are almost 8% of GDP , still India holds a low position in the international insurance sector. And one of the main obstacles which is still restricting the growth of the Indian insurance sector is “Lack of Awareness”.

More than three-fourth of India’s insurable population has no life insurance. Many People are illiterates, they don’t have complete knowledge of any insurance policy and its benefits. Sometimes these people buy rumours about insurance being a death policy and only be claimed after death which decreases their interest towards it. But “Lack of awareness” is not the only problem that is needed to be tackled , there are more than 45% people living below poverty line and they cannot even think about insurance as they don’t have that much money to pay the premiums to secure their life and properties and here MICROINSURANCE comes into the picture .

“What happens when a lonely earner of a poor family dies? ,What happens when a child from poor background gets disabled or hospitalized? , What happens when the crops gets destroyed by the natural calamities like floods and droughts or the home of a family gets destroyed by fire or any natural disaster in rural area? This is the time when they need micro insurance”

But the issue arises is the unavailability of insurance companies in rural areas which creates a gap between the demand and supply of microinsurance . According to the reports , 17 of the respondents out of 100 are still unaware about its benefits . But with the help of NGO’s/SHG’s , IRDAI is trying to reach the “the untapped areas ” at relatively very low cost.

But this graph of the indian insurance sector is much better and developed than the newly arisen insurance sector. In April 2000, the Insurance Regulatory Development Authority (IRDAI) came into existence to regulate the insurance industry. The mission of IRDAI is “to protect the interests of the policyholders, to regulate, promote and ensure orderly growth of the insurance industry and for matters connected therewith or incidental thereto”. And after the establishments of reforms related to privatization and liberalisation, the industry started to run in the race . According to the experts , the insurance industry in India now contributes 4.5% of national GDP but they have also ruled out the possibility that the sector can contribute up to 10% of GDP. According to IBEF’s (Indian brand equity foundation) latest report, the overall insurance industry is expected to reach the US $280 billion by 2020.

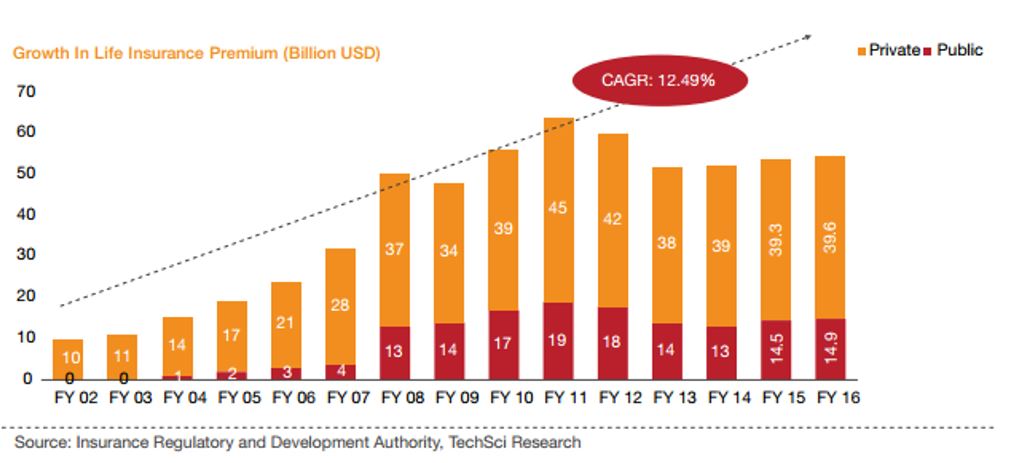

PREMUIM RATES

Life premiums which are the one of the source

of the industry to earn profit are predicted to reach US $230 billion by 2025 ,

driven in apart of culture of saving .

According to march 2016 reports , the rising

participation of private sector has led

to increased their share in insurance industry , with the market share of 39.6%

in FY16 as compared to zero in FY03. Developed countries like UK have better

quality of life as compared to India.

That means the risk of getting prone to diseases , infections which

could result in death of the insured is very less in UK as compared to India

and therefore it is not feasible for insurers to charge higher rates of

premiums in such country with comparatively low risk. But in India the premiums

are relatively low as the health insurance sector has not permeated through

much of the population and higher rates would further discourage people from

getting themselves insured. And hence the insurance industry in India is not

able to collect huge amount of premiums and are slightly moving towards the

loss.

GOVERNMENT INITIATIVES

And the new government and IRDAI are bringing up new reforms which is helping industry to grow rapidly . One of the initiative is, that government has approved to increase the FDI (Foreign direct investment)limit from 26% to 49% in insurance sector which would help to attach investment in the sector so that the company can rebalance its expenses .

In 2017, insurance sector in India saw 10 mergers and acquisition(M&A)deals worth US $93 million and enrollments under Pradhan Mantri Suraksha Bima Yojana (PMSBY) reached 130.41 million in 2017-18. Then under the budget 2018-19 , National Health Protection Scheme under Ayushman Bharat which provided insurance cover up to Rs. 5,00,000 to more than 100 million vulnerable families in India. In April 2017, IRDAI started a web portal – isnp.irda.gov.in that allows the insurer to reach their customers through the technology since people are more active there and allow them to sell and register policies online and providing the whole knowledge of the upcoming policies and their benefits.

But this couldn’t solve the whole problem, the motor insurance (Non life insurance) is rapidly growing as compared to life insurance . The General insurance market/Non life insurance is about Rs.11000 crores and with the expected growth in the Indian economy and new players moving in, the market for general insurance is expected to grow at 18% per annum. Over the last ten years, the compounded average growth rate for the industry works out to more than 15%. Whereas considering that only about 65million out of 250 million people are covered by life insurance.

“So let me get this straight, you have insurance for your cell phone but not on your life?”

TERRORISM INSURANCE

“But in this unstable world, do you really think life insurance and general insurance is enough to face global risks like terrorism ?”

As these risk increases we also need an optimal solution for it . The multinational companies need to understand their exposures and be confident that they have an appropriate risk management programme in place.

Across the world , the terrorist insurance market was originally established to respond to bomb attacks , but the 2017 data highlights the changing face of terrorism : cover must evolve to respond to these low technology incidents , where there may have been little or no damage .

Indian Insurance products are also needed to address the rising level of cyber terrorism and malicious threats or acts where the motive is unclear and a national terrorism insurance programme is either unavailable or will not cover the incident. There also have been increasing demand for political risk insurance. The impact of terrorism, political risk and violence are that the people keenly want to secure their properties, assets, revenue generation and supply chains. Ultimately the clients of the insurance industry want the industry to ensure them that they will provide genuine support to their clients by protecting them against the threats that exist in an increasingly unstable world.

CONCLUSION

Yes, the Indian insurance sector is growing but it still requires a lot of innovation speciality in the products being offered, insurers also need to participate actively and need to develop action plans that will position them to become market leaders . We need Artificial Intelligence (AI) and InsureTech at a broad level to improve productivity and personalisation.

With the increase in awareness level about the insurance and its products, the day is not so far when all the insurable population in the country would have been brought under the insurance domain…

This article has been written by: Sharniya Sachin.

Comments 2

Related Posts

Surety Bond: How Do They Actually Work & Actuarial ConsiderationsDefining Microinsurance | An untapped marketGroup of Actuaries and Investment Officers to study index-linked products in IndiaApplication and Challenges of Machine Learning In Insurance Sector

Pingback: My Homepage

Insurance can people solution.